The Energy Transition is the largest capital deployment in history, with c.$2T spent annually in 2024 and forecast to rise to c.$4T annually by 2030. The scale, in terms of absolute $ spent, dwarfs all other notable investment trends today.

Aside from the size, energy is foundational to economic activity making this a theme that extends well beyond the basic activity of how we generate and deliver electrons, and one that touches on all other sectors.

The dimension of the opportunity, its broad impact, and the fact that technology and regulation are coalescing around the most attractive opportunities today, makes a live investment strategy for this space fundamental for any asset allocator.

And yet, the flipside of that scale and impact is the reality that energy is an overwhelmingly broad space for investors to get their head around. The complex interplay of technology, regulation, and geopolitics often deters investors from making active investment decisions in this area.

This primer is designed to equip investors with a full toolkit to overcome that complexity and engage with the Energy Transition.

On this page, you'll always find a brief summary of our structural investment thesis and top 3 focus areas. Behind that, you'll discover a growing library of deeper material for those looking to dig into our views:

- Value Chain Deep Dives-providing investment overviews of different verticals

- Investor Tools-such as due diligence lists and portfolio construction guides

- Case Studies-providing investment lessons to apply to incoming investment evaluation

- Recommendations-covering live public and private market opportunities

- Explainers-digging into timely discussion points such as this

What matters in Energy Transition investing?

For investors coming to the space fresh, there are some important principles which should be borne in mind when evaluating any new energy investment.

1) Capital Intensity

Building energy infrastructure in the physical world absorbs massive amounts of capital, hence why we're already at that $2T/year spend. Related to this fact, project and industry timelines are long, often stretching over years and decades as opposed to the fast product cycles seen in tech, for example.

2) Leverage

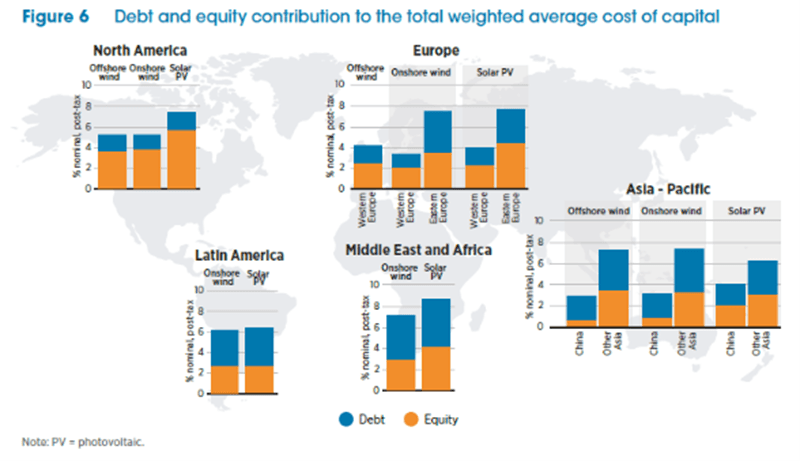

Funding all of that capex is impossible without debt, with energy projects often exceeding 100% debt:equity ratios.

Figure 6: Debt and equity contribution to the total weighted average cost of capital by region and technology

3) Lack of pricing power

Energy industry actors throughout the value chain frequently participate as price takers in auction markets.

4) Lack of IP

There is little defensible IP in energy markets; this is partly related to the long project cycles which inherently prevent the rapid commercialisation of innovative technologies, and the network effects which would then accrue. Instead of IP, competitive commercial advantage is often determined by first-mover advantages related to scale, siting, regulatory relationships, and contracts.

5) Exposure to consumer regulation

Every dollar spent in this industry ends up on a consumer-facing bill. Therefore, every investment in this space is exposed to the changing whims of political and public opinion. If an investment is likely to contribute to energy costs rising above inflation, it will eventually attract regulatory intervention.

Of course, individual investment opportunities will have differing levels of exposure to each of these factors. But, putting these characteristics together should give investors a strong sense of what to expect as the norm in this segment and the potential risks. Energy investors frequently contend with cyclicality, earnings volatility, modest return profiles (ROCE) at individual asset level, and regulatory breaks (both positive and negative).

Understanding durability of future equity cash flows, in the context of a financially levered investment universe, is crucial.

In public markets, this creates wide intra-sector dispersion, with the performance differential between the top and bottom decile of energy stocks >70% in 2024.

In private markets and earlier stage investing, this manifests in a high failure rate, with cash runway an essential metric. For example, between 2018-24, nearly 40% of cleantech VC deals failed to raise a follow-on round.

Our Energy Transition Investment Thesis

Despite these realities, we believe that Energy Transition remains an investment theme that demands an active allocation.

Why? First, the timing and scale of the opportunity.

Without succumbing to the trope that 'this time is different', it is true that today we are seeing a convergence of technologies, geopolitical incentives, and economics which dictate that we will fundamentally reshape the way we deliver energy over the next decade.

The fact that utility-scale solar is the lowest cost and fastest to deploy new generation source is not going way. Nor, is the fact that the economy is electrifying leading to demand growth - be that from EVs, factories, or data centers. And, while political winds can change course rapidly, greater domestic investment in energy infrastructure is a given everywhere - even if the underlying motivation, be it climate change, energy security, or economic enablement, will vary by country.

Energy Transition Investment Growth by Category

Annual investment in billions USD across key energy transition categories (2020-2030)

These structural trends give us confidence in underwriting the fact that the scale of investment in this area will continue to dwarf most other alternatives. The flipside of the capital intensity and lengthy projects we discussed earlier is that, once investment trends are embedded in this space, they tend to remain resilient. And, given, the rules and regulations governing outcomes in many areas are forming today, we believe that many of the next decade's breakout investments will be first movers today.

Second, that long-duration cyclicality is in itself an attractive opportunity for active investors, providing multiple entry and exit points for informed investors who can allocate tactically while understanding the durable nature of the strategic trend.

Third, the dispersion offers real alpha to active investors. Given the attributes of the sector as a whole, this is not a space where we would advocate a blanket allocation through broad ETFs for example.

Fourth, this is a deep, liquid, varied investment segment compared to most others. Available instruments span public and private markets, equity and credit, project finance to broad ETFs, commodities and more. This variety means that it is possible to tailor exposure to explicitly cater for an investor's mandate and risk appetite.

Lastly, there is a diversification opportunity here. The drivers of this sector tend to be commodity prices, regulation, and interest rates. That can make investment opportunities a useful adjunct for broader investment portfolios, especially given the range of instruments available as just mentioned.

Investment Focus Areas

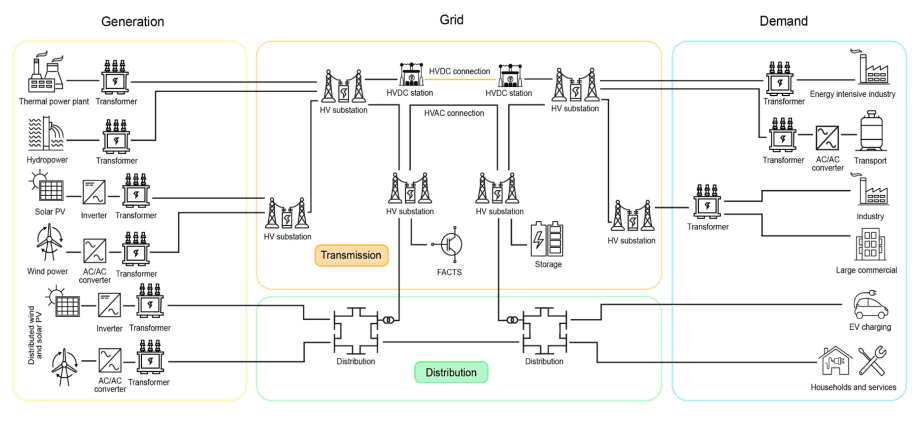

The 2 core parts of the Energy Transition value chain are 1) Power Generation, and 2) Transmission & Distribution. Upstream is the supply of raw materials and commodities, and downstream are the end-uses such as EVs.

Technical diagram of the complete power system value chain from generation through transmission and distribution to end-use sectors

At the value chain level, the Energy Transition means that this system needs to move from one that takes in fossil fuels, delivers energy on demand at a marginal commodity cost, and has a centralised distribution network; to one that takes in a different set of commodities such as rare earths, delivers intermittent energy at zero marginal cost, and does so across a fragmented distribution network.

While the below is not a laundry list of the best ideas in Energy Transition, we believe most investors will benefit from starting a core allocation to the space in the following 3 areas across different value chains:

1) Grid modernisation hardware and software (Transmission & Distribution)

This represents the largest opportunity of the next decade in our view. While the last decade was about falling costs of supply and new sources of demand, such as EV, the biggest bottleneck we see today is the inadequacy and age of the current grid system across much of the US and Europe. It is this inefficiency that takes a source of power that costs nothing at times, and manages to still deliver unaffordable consumer prices. Relieving bottlenecks, redesigning grid systems, and ultimately reducing consumer transmission costs is our most important theme and our top core allocation today.

Specific ideas are discussed here.

2) Firming Solar (Power Generation)

The LCOE of solar puts this as the most investable source of medium-term new supply and growth in most markets. Already cheaper than alternatives, and still getting cheaper, solar will continue to hold the mantle as the core new power generation technology globally over the next 5-10 years.

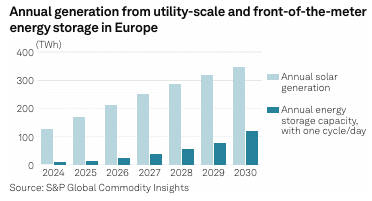

While this trend endures, the real challenge of the next decade is 'firming' the intermittent supply we get from solar. That means slowly ratcheting up the load factor on solar from the c.25% to c.40% and beyond. What will that take? Storage (lots of it), but also developments in panel technology, site optimisation, and grid integration.

Annual generation from utility-scale and front-of-the-meter energy storage in Europe (TWh)

3) Green Steel (End Use)

We believe the next decade will see one of the major industrial verticals make a breakthrough in terms of electrification and decarbonisation. At this stage, the most promising is Green Steel (discussed here).

We would not claim that these 3 are the only interesting or viable Energy Transition investments - far from it. As you dig deeper through our material, you'll find detailed analysis of opportunities outside of these and how we see those fitting in a broader allocation.

Nevertheless, we would still advocate starting here.

You will also note that there is no mention of the upstream commodity inputs in our 'top 3'. Our rationale is that there will be interesting valuation driven tactical or hedging opportunities in that space, but that it is unlikely to take a central allocation for most strategic investors.